Welcome to this special weekend edition of A Ticker A Day, which is available to all subscribers free and paid and will hopefully give a flavor for how I do my analysis. In today’s episode I’m going to take a look at Casper’s IPO filing.

Casper (www.casper.com) is a direct-to-consumer (DTC) product company that sells mattresses, comforters, pillows, sheets, and even dog beds. In full disclosure I love their products, and have been a loyal customer for some time.

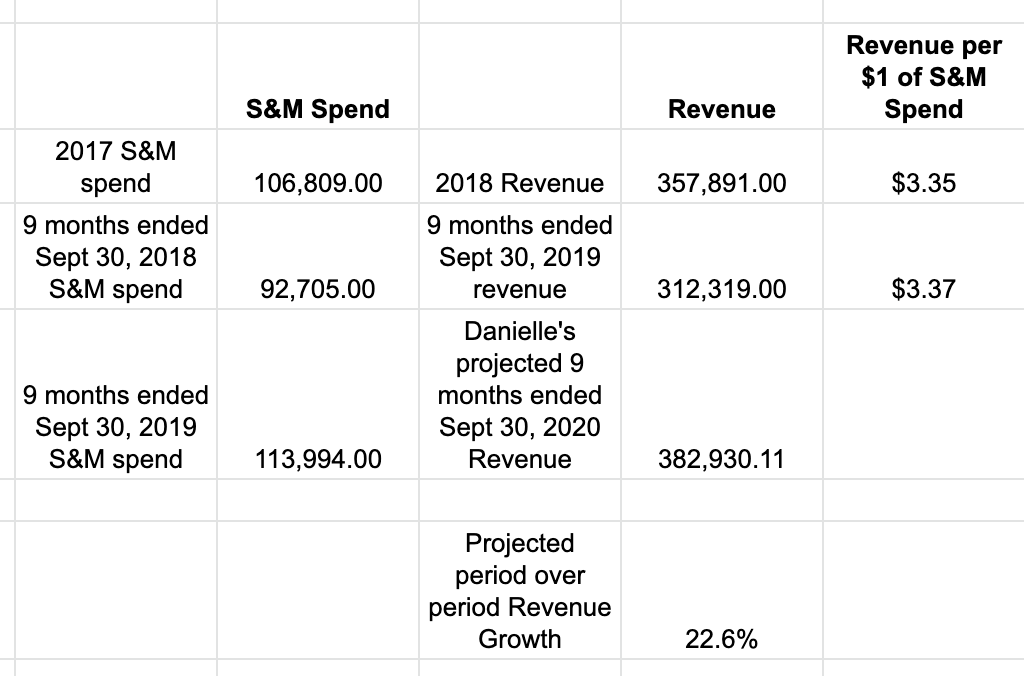

The company is not profitable, with a net income loss of $67.3 million in the 9 months ending Sept. 30, 2019 on $312.3 million of revenue. Compared to revenue of $259.7 million for the same period of the prior year, the business is growing the topline 20% year-over-year. While net loss per dollar of revenue (something you have to calculate, it isn’t in the filing) declined 15% between the two periods from -$0.25 to -$0.22.

Most venture-backed consumer startups enter the public markets with losses, the common wisdom being that they could cut expenses and become profitable at anytime but that it is better to invest in growth and market capture in the early days.

The company’s balance sheet shows $54.9 million of cash as of September 30, 2019 and net cash used in operating activities of $29.7 million for the 9 month period leading up to that date. Dividing that net operating cash across 3 quarters evenly, the company’s burn rate is ~$10 million per quarter (and on an improving trend), giving the business an implied 5.5 quarters of runway on existing cash. Of course, this is a product business carrying inventory and this is only showing the net cash figure. The amount of cash on hand needed for operations is a little less clear. Notably, the company has $15.9 million in short-term debt, which may be a revolving line typically used to finance operations in company’s like this.

The bulk of the company’s spending is going towards sales and marketing, and some may wonder whether they should be getting better ROI on their spend for a higher growth rate. However, when I assume there is some lag in S&M spend generating sales (maybe not a whole year, but we don’t have more granular data to work with) it appears efficiency has improved slightly, which could accelerate year-over-year growth.

What I’m Doing

For now, I’m going to watch and wait.

I like seeing 50% gross margins and a fairly stable revenue per dollar invested in S&M. It suggested a health capital allocation machine has been built to drive sales. I would need to see continued improvement to the efficiency of sales & marketing spend, which would translate to accelerated growth rate. I would also like to see a continued decline in the quarterly net cash requirement.

The decision to buy into this stock today (hypothetically, since it has not priced yet) versus the decision to buy in 5 years from now should be roughly the same. It looks like the company has at least a year of its own runway at the current burn, and raising $100M would give it at least a year more. So the question really is: can this company raise enough and reduce burn enough to give it the runway it needs to get to profitability? Assuming they float 5-10% of shares, a second offering to raise more in 9-12 months wouldn’t surprise me.

What I’m Watching

Price discovery on IPOs is really difficult. I feel like there are really only two great times to buy an IPO: before it goes out (be part of the book) and right before the first earnings call (assuming you think it will go well). This is because there is still so much unknown information for the outsider retail investor who has not seen the road show. Small float, potentially several tranches of lockup periods that will need to expire, unclear whether larger VC investors will hold or sell upon liquidity.

I didn’t invest in the company, so whether it prices above or below the current private market valuation doesn’t matter to me, but I also don’t have the same amount of information as an existing investor, employee or roadshow buyer. So I’ll wait until I am at less of an information disadvantage.

If anything, it will be interesting to watch the short selling of this stock (which won’t really pick up until the 30 day limit on lending shares for shorting expires) and the potential for a short squeeze to drive up the price on such a small float. See the Square IPO for a fascinating recent example of this playing out.

Reading List

Casper files to go public, shows you can lose money selling mattresses (Alex Wilhelm, TechCrunch)

These are the unusual, colorful slides that mattress startup Casper is using to convince IPO investors that it can capitalize on the $432 billion 'sleep economy' (Business Insider)

Thank you for a great first week! We will start again on Monday with Aarons Inc ($AAN). If you have opinions, resources, thoughts, etc. on this stock please feel free to reply to this email.

Disclaimer: You understand that by reading “A Ticker A Day” you are not receiving investment advice. No content published here constitutes a recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. You further understand that the author(s) are not advising you personally concerning the nature, potential, value or suitability of any particular security, portfolio of securities, transaction, investment strategy or other matter. To the extent that any of the content published may be deemed to be investment advice or recommendations in connection with a particular security, such information is impersonal and not tailored to the investment needs of any specific person. You understand that an investment in any security is subject to a number of risks, and that discussions of any security published on “A Ticker A Day” will not contain a list or description of relevant risk factors. In addition, please note that some of the stocks about which content is published have a low market capitalization and/or insufficient public float. Such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information.

“A Ticker A Day” is not intended to provide tax, legal, insurance or investment advice, and nothing published here should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security by its author(s) or any third party. You alone are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should consult an attorney or tax professional regarding your specific legal or tax situation.

A Ticker A Day - Weekend Edition: Casper ($CSPR)